Introduction

France is the leading European country regarding agricultural production and acreage and one of the leading exporters of agricultural commodities in the world (Insee Première, 2015). Over time, France has decided to encourage the coverage of several kinds of agricultural risks, by using tools offered by the Common Agricultural Policy (Cap). The Cap evolutions in 2009 and 2014 have also allowed a cofinancing of risk management instruments. France has used the possibilities open by the Cap Health Check to provide a subsidy amounting to 65% of premiums by using funds from the 1st pillar.

Therefore, in recent years, the panel of risk management instruments available in France has been growing, now including a wide range of crop insurance policies, mutual funds and precautionary savings.

- Sanitary risks are now hedged through a mutual fund for health and environmental risks in agriculture (Fmse - Fonds de Mutualisation des risques Sanitaires et Environnementaux). This fund in which participation is compulsory has been created in 2012 and its scope is increasing.

- Weather risks are hedged through crop insurance policies. For more than 50 years, French farmers have benefitted from an insurance system which hedges against natural disasters. In 2005, the reform of crop insurance and the introduction of private multi-peril crop insurance policies drove to a change of paradigm.

Despite this strong development encouraged by quite high subsidization levels, participation to some of these various instruments remains at a low level with significant disparities among specializations (Enjolras and Sentis, 2011; Bardaji et al., 2016). This observation has been noticed in the literature and is common to all European countries, among them Italy (Enjolras et al., 2012; Santeramo et al., 2016).

As a result, many ways have been explored to foster the subscription of agricultural insurances. These considerations have resulted in the creation of a baseline insurance policy, the “contrat socle”, designed to hedge less losses while covering more hazards and more farms.

This article is organized as follows. In the first part, we describe the current situation of crop insurance in France, which explains the motivations to reform crop insurance policies. In the second part, we detail the functioning of the new baseline crop insurance policy. In the third part, we conclude by discussing the stakes associated to this kind of policies.

The current situation of crop insurance policies in France

Before any regime in favor of crop insurance was launched, the French government used to compensate losses on a case-to-case basis. A severe draught led to the creation of a public compensation fund in 1964 whose aim was to hedge against natural disasters. Premiums were shared equally between the government and farmers.

The development of the private insurance market was accelerated starting from 2005 when the French government decided to push private insurance by subsidizing premiums. Starting from 2010, risks covered by insurers are excluded from the public compensation fund (Fngra – Fonds National de Gestion des Risques en Agriculture).

Climatic hazards hedged by crop insurance now include: frost, hail, sunburn, excess precipitations, excess temperature, flooding, heavy rain, drought and storm. Many productions are concerned by this coverage: cereals, oilseeds, protein crops, industrial crops and vines. Starting from 2016, grassland is also concerned.

Insurance policies can be sold:

- 'Crop by crop': All plots of a given insured crop have to be included in the policy. To receive a claim, the loss must exceed 30% of an historical average (three last years or Olympic average). The deductible can be fixed between 30% and 50%.

- 'At the farm level': In that case, the farmer insures more than two crops representing at least 80% of cultivated acreage. The deductible is then lowered to 25%.

These policies can be subsidized up to 65%. In that case, 75% of the subsidy is provided by the European Agricultural Guarantee Fund (Eagf) and 25% by the Fngra.

For the period 2014-2020, France took the opportunity given by the EU Commission to transfer credits associated to risk management from the 1st to the 2nd pillar. This choice was motivated by higher flexibility and selection of measures offered in this new framework (crop insurance, mutual funds). 2nd pillar allows for pluri-annual planning, which grants more visibility to risk management instruments, while not changing the fundamentals of instruments already existing such as crop insurance.

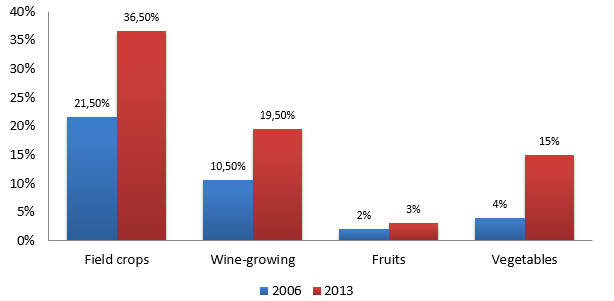

However, between 2010 and 2015, crop insurance has mainly concerned field crops and, to a lesser extent, wine-growing and vegetables (Figure 1). In recent years, participation rates did only increase very slightly. In 2013, 75 833 multi-peril crop insurance policies were subscribed in France according to the Programme National de Gestion des Risques et Assistance Technique 2014-2020 (Pngrat)1.

Figure 1 - Evolution of insured areas in France for some productions

Source: French Ministry of Agriculture (Pngrat)

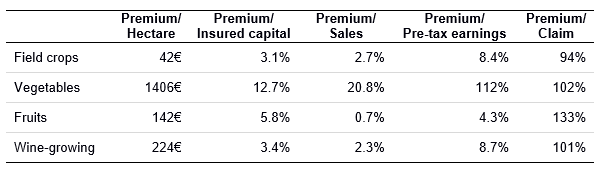

The crop insurance system faces heavy limitations which explain the current situation. The first one is that only 30.6% of cultivated agricultural areas were insured in 2013 (27% in 2010). The second one is the ratio between premiums and claims which has been unbalanced since 2005, especially over the most recent years. The third one is the heavy cost of insurance compared to the financial capabilities in some sectors (Table 2).

Table 1 - Weight of insurance premiums according to different criteria

Source: French Ministry of Agriculture (Pngrat)

Development of a baseline crop insurance policy, the “contrat socle”

In order to overcome the different limitations explained above, the solution that is generally adopted is to develop the range and scope of insurance policies. A paradigm is provided by the United States which have progressively increased the range of insurance and guarantees (Glauber, 2014). A ‘natural’ extension of the existing insurance program would have been to hedge directly price risk, through the introduction of farm revenue insurance. This solution was not adopted for two main reasons. The first one is the cost of subsidies for the government, which would have been multiplied by at least five considering existing participation levels. The second one is the fact that there is no guarantee that participation would have increased mechanically with the introduction of such new policies, the latter being probably more expansive for farmers.

For these reasons, the French government, together with farmers' unions and insurers, decided to operate a strategic change starting from 2013 and to adopt an original way. Instead of developing more complex products, the main aim of public policies is now to hedge the maximum number of farms at a lower cost for farmers and the government. The instrument for this policy is a newly structured crop insurance policy named “contrat socle”, which provides a kind of baseline guarantee against climatic shocks, still focusing on crop yields. By contrast with other experiences in the world, the principle is to increase significantly farmers' participation in the crop insurance system by decreasing the amount of premiums and the coverage.

Instead of hedging yields by compensating the farmer for the average sales value of its produces, the “contrat socle” hedges only the value of production costs. Claims are therefore designed not to compensate the selling value of the production, but rather to help farmer start again their activity and even to start a new production cycle. In practice, the premium and the indemnity are computed on a per hectare basis for a given production and location. After some experiments with winegrowers starting from 2012, the policy was defined in collaboration with all public and private stakeholders in December 2015 and launched starting from mid-January 2016. Four sectors are mainly concerned: wine-growing, field crops, grasslands and fruit production.

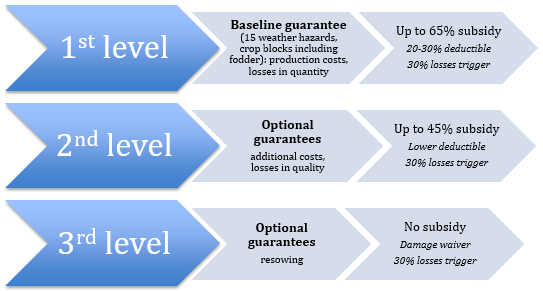

The standard structure of a 'contrat socle' is the following (Table 2):

- A first level hedges only against production losses (fixed and variable expenses) at the crop scale. Production costs follow a scoring grid, which is fixed each year by Chambers of Agriculture and experts, and validated at the national scale. No guarantee is then provided on yields and selling prices with the first level. The trigger amounts to 30% of losses while the deductible is equal to 30% of losses (except for grasslands, 25%). If all productions are insured, then the deductible may drop to 20%. Following the EU regulation, this first level is subsidized at a 65% rate.

- A second level hedges against yield losses at the farm or at the crop scale, by complementing the first level, e.g. with a deductible rate decreased to 25%. This level can be customized but subsidies are capped at a 45% rate. Farmers can then find a coverage similar to the pre-2016 situation and to common crop insurance policies protecting yields.

- A third level proposes additional guarantees, such as variations in prices and quality losses. This level does not benefit from any subsidy.

Figure 2 - Summary of the structure and features of the "contrat socle"

Source: Own representation

According to simulations from the insurers, the premium of an insurance policy in field crops amount to approximately 28 euros per hectare without subsidization for the first level, as opposed to 36 euros per hectare before (actual second level) with a standard multi-peril crop insurance (-22%). The cost amounts to about 10 euros per hectare after subsidization.

Conclusion: remaining challenges for farm risk management in France

For its first year of operation, the new baseline insurance policy does not seem to have increased the farmers’ participation. Yet, severe flooding and hail episodes during summer 2016 across the entire country made thousands of farmers discover the financial consequences for not being insured. This situation emphasizes the need to improve communication regarding the “contrat socle”, by explaining the functioning of the policy and its advantages.

In the future, if both the government and the insurers manage to increase participation (the target for the participation is fixed to 70% of farms), then the way may be paved for future improvements, such income stabilization tools. At the moment, only some experiments for revenue insurance are being imagined, especially in the fruit sector, which is very sensitive to both yield and price risk2. Extending the scope of insurance policies supposes to increase public funding, which is a rude challenge for a country such as France that needs to restore budgetary balances.

The conjunction of increased risk hedging, associated to increased public financing, and the challenge of farmers participation is making uncertain the final outcome of this process, while instability of yields and prices increases. A situational analysis is scheduled to be performed starting from 2017.

References

-

Bardají I., Garrido A., Blanco I., Felis A., Sumpsi J.-M., García-Azcárate T., Enjolras G. and Capitanio F. (2016), "State of Play of Risk Management Tools Implemented by Member States During the Period 2014-2020: National and European Frameworks", Report for the European Parliament, 146 pages

-

Enjolras G. and Sentis P. (2011), "Crop insurance policies and purchases in France", Agricultural Economics, 42(4): 475-486

-

Enjolras G., Capitanio F. and Adinolfi F. (2012), "The demand for crop insurance: Combined approaches for France and Italy", Agricultural Economics Review, 13(2): 5-22

-

Glauber J.W. (2013), “The Growth of the Federal Crop Insurance Program, 1990–2011,” American. Journal of Agricultural Economics, 95(2): 482–488

-

Insee Première (2015), "L’agriculture en 2014 en France et en Europe", n°1560, 4 pages

-

Santeramo, F.G., Goodwin, B.K., Adinolfi, F., Capitanio, F. (2016), "Farmer Participation, Entry and Exit decisions in the Italian Crop Insurance Program", Journal of Agricultural Economics. 67(3)