|

Versione italiana |

Introduction

The Common Market Organisation (CMO) for fruit and vegetable products is currently evaluated by the European Commission. The evaluation may lead to a reform of the CMO, for instance for processing tomatoes, one of the most heavily subsidized sectors in primary production of fruit and vegetables. The current production subsidy equals approximately 50% of producer turnover. The European Commission considers reducing the production subsidy for processing tomatoes and replacing the subsidy by area payments. This paper evaluates two possible reforms of the processing tomato supply chain: (1) an abolishment of the production subsidy and (2) a replacement of the production subsidy by area payments (decoupling). The evaluation focuses on the impact the reform may have on production and trade patterns of fruits and vegetables in Europe.

Simulation analysis

This paper analyses two possible reforms:

1 - the abolishment of the production subsidy without a compensation in terms of an area or any equivalent payment;

2 - the abolishment of the production subsidy with partial compensation in terms of an area or an equivalent payment. The area payment is assumed to prescribe the allocation of some land to the production of processing tomatoes in order to prevent unfair com-petition for growers of other vegetables, fruit and arable crops.

The impact on production and trade is estimated using HORTUS, a supply and demand model for production and trade in fruits and vegetables in the European Union (Bunte and Roza 2007).

The impact of a reduction in the production subsidy

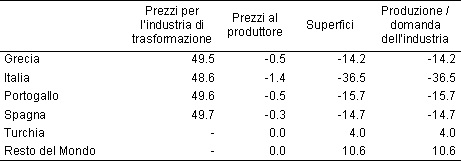

The abolishment of the production subsidy causes an upward shift of the supply function of processing tomatoes. Growers of processing tomatoes will shift their acreage to other crops in their building plan. They will grow processing tomatoes less often. Assuming slightly upward sloping supply curves at the national level and a price inelastic demand for proc-essing tomatoes, the abolishment of the production subsidy will be met by an increase in the prices the processors pay for processing tomatoes (Table 1). The price increase is not so much due to the ability of growers to set prices, but to their supply behaviour. They simply reduce supply. Grower prices fall slightly. Given the elasticities chosen, the de-mand for (European) processing tomatoes and thus the output of the tomato processing industry will fall by approximately 15% in Greece, Portugal and Spain and by more than 35% in Italy. Turkey and the Rest of the World will be able to increase imports into the EU and as a result their production.

Table 1 suggests that Italy will face the largest drop in output of processing toma-toes. Italy is a large importer, exporter and re-exporter and will face a surge in imports from the Rest of the World in its home market. Italy is also by far the largest exporter to non-EU countries and faces a major decrease in its exports to these markets. For Greece, Portugal and Spain, domestic demand is the most important driving factor. This shelters their domestic production to some extent.

Table 1 - The impact of scenario I on the processing tomato supply chain (percentage changes)

What is even more important is the fact that agricultural production will lead to a production shift towards all other crops. In Greece, Portugal and Spain, the area allocated to other crops grows moderately by 0.2-1.0%. In Italy, the area allocated to other crops grows by 1.6-1.8% (see Table 2). As a result of the growth in Mediterranean crop produc-tion, North European countries will face fiercer competition in the production of fresh fruits and vegetables. Mediterranean countries gain market share in North European import markets (Bunte and Roza 2007). However, the overall impact on North European produc-tion is negligible.

Table 2 - Area development in Europe under scenario 1 (percentage changes)

The impact of decoupling

In this section, we discuss the impact of a subsidy reduction plus the introduction of area payments. We assume that area payments prescribe the allocation of some land to process-ing tomatoes in order to prevent unfair competition with producers of other vegetables, fruits and arable crops. The impact of area payments is modelled by assuming that the land allocation in the countries producing processing tomatoes adjusts partially to the price in-centives implied by the subsidy reduction.

Land allocation adjusts partially to the price incentives implied by the reduction in the production subsidy and the associated fall in demand. Because land allocation does not adjust fully to the price incentives a gap arises between area and output developments. Output falls much harder than land (Table 3). Because land use for processing tomatoes becomes more extensive, growers of processing tomatoes will employ less labour and capi-tal. The resulting reduction in capital and labour costs will lead to a fall in grower prices due to sharp product competition. The basic difference between scenario I and scenario II is that under scenario I, growers of tomato processors are able to shift the burden of the price reduction to the producers of other crops by switching crops. In scenario II, the bur-den of the fall in grower prices falls primarily upon the growers of processing tomatoes.

Table 3 - The impact of scenario II on the processing tomato supply chain (percentage changes)

The partial adjustment in land allocation and the impact on grower prices have major consequences for growers’ substitution behaviour in the Mediterranean area. Growers of processing tomatoes will switch to arable crops and extensive vegetables production rather than fruits and fruit vegetables. Growers of processing tomatoes remain stuck in the production of arable crops and extensive vegetables and within this category they switch to products like onions, carrots and potatoes, but probably also to cereals, sugar beets and oil seeds. As a result of this lack of substitution behaviour in the Mediterranean area, North Europe is hardly influenced at all (see Table 4).

Table 4 - Area development in Europe under scenario 1I (percentage changes)

Conclusion

In 2006-2007, the European Union evaluates and possibly amends the Common Market Organisation (CMO) for fruits and vegetables. One of the principal elements of the current CMO is a production subsidy for processing tomatoes. The European Union considers re-ducing and decoupling the subsidy for processing tomatoes. This report evaluates what the likely impact is of these changes on production and trade patterns for fruits and vegetables in the EU. Abolishment of the production subsidy has the following consequences:

- the reduction in the production subsidy is likely to be passed through into higher input prices for tomato processors.

- Demand for European processing tomatoes will fall by 15% in Greece, Portugal and Spain and by more than 35% in Italy. Demand for European processing tomatoes may fall harder, if imports from non-European production areas rise faster.

- Mediterranean farmers will switch production from processing tomatoes to fresh fruit and vegetables.

- In North Europe, Mediterranean exporters crowd out domestic producers to some ex-tent.

If the abolishment of the production subsidy is compensated by area payments, the above results change into the following results:

- Grower prices fall substantially. Mediterranean growers do not adjust their land alloca-tion fully in order to collect area payments.

- Mediterranean growers switch to vegetables in the open and arable crops. North Euro-pean production is hardly influenced.

Basically, the paper stresses that the Mediterranean countries have a comparative advan-tage in the production of fresh fruit and vegetables rather than processing tomatoes. A reduction in the production subsidy for processing tomatoes will lead to a shift in produc-tion in the Mediterranean towards this advantage. In policy terms, processing tomatoes are the Mediterranean’s defensive interests and fresh fruit and vegetables the Mediterranean’s offensive interests. Area payments with restrictions on land use countervail the develop-ment towards comparative advantage. Area payments lower the adjustment burden for growers of processing tomatoes but at the cost of lower grower prices.

References

- Bunte F., Roza P. (2007), Peeling tomato paste subsidies, The Hague: LEI, in press.